Trucking Rates Soar To Highest Level Since 2022 While 15,000 Carriers Fight To Survive

The Logistics Managers Index posted transportation prices at 71.4 in January 2026, the fastest rate of expansion and the highest reading for this metric since April 2022. Nearly four years of freight recession, and the pricing needle finally moved. Except that truckload volume remains well below pre‑recession peaks and still materially below late‑2024 levels, even as rates rise. Prices are surging while demand stays crushed. That contradiction tells a bigger story than any recovery headline. Everyone sees the rate spike, but almost nobody is tracking where the missing volume went, or what happens when shippers find cheaper alternatives already waiting for them.

Scarcity Engine

Rates didn’t climb because freight is booming. They climbed because trucks disappeared. The freight recession that began in 2022 is one of the longest and most disruptive in modern trucking history, systematically eliminating carriers through bankruptcies, consolidations, and financial exhaustion. Fewer trucks chasing fewer loads created artificial pricing power. The Outbound Tender Reject Index rose from around 4.3% in early September 2024 to roughly the mid‑5% range by late February 2025, confirming carriers had begun to regain some leverage off the bottom. But that leverage came from scarcity, not strength. The surviving carriers aren’t healthier. They’re just the last ones standing.

Grocery Math

For shippers moving consumer goods, the math changed overnight. Trucking rates are widely forecast to increase modestly, in the low single digits, in 2026 if trade policy stabilizes, on top of years of accumulated cost pressure. Warehousing utilization bounced back to 54.4 on the LMI as companies rushed inventory ahead of tariff deadlines. Every pallet that moved early moved at a higher rate. Families won’t see “transportation prices” on a receipt, but they’ll feel it in grocery aisles where logistics costs get baked into shelf prices without a label.

Shipper Revolt

Shippers aren’t quietly absorbing these rates. They’re pivoting from chasing the cheapest spot rate to locking in reliable capacity through contracts and increasingly routing freight entirely away from trucks. Intermodal and ocean alternatives are gaining share on long‑haul lanes as cost‑conscious logistics managers hedge against trucking price exposure. The shift is strategic, not reactive. Shippers watched years of freight chaos and decided the answer is diversification. That means every truck sitting empty at a loading dock represents a shipper who already found another way.

Ocean Escape

Ocean freight rates peaked in 2025 and are widely forecast to decline by around or more than 10% across major trade routes in 2026. Read that again. Trucking prices are at multi‑year highs. Ocean rates are falling into the double digits. The price gap between modes just became a canyon. Shippers with any flexibility on delivery timelines can route long‑haul freight to water and save substantially. One commodity market is recovering while its closest competitor is getting cheaper. That kind of modal arbitrage doesn’t just nibble at trucking volume. It restructures supply chains.

Connected Collapse

Here’s what ties every one of these ripples together. Pricing is now decoupled from volume. Trucking rates rise because capacity is scarce. Shippers flee to cheaper ocean freight. That pulls volume from trucking. Fewer loads are spread across fewer trucks. Carriers keep pricing power but lose the freight to fill their trailers. Ocean rates fall. Trucking rates climb. Shippers shift more freight to water. Same mechanism. Different quarter. Identical result. The system feeds itself, and every cycle leaves the trucking industry smaller and more brittle.

Survival Calculus

“I just think the survivability of this current market diminishes substantially,” warned Dean Croke, principal analyst at DAT iQ. Tens of thousands of truckers face compressed margins despite those headline pricing gains. After years of recessionary conditions, the carriers still running didn’t emerge stronger. They emerged depleted, with burned‑through savings and equipment they can’t afford to replace. Every load is a survival calculation: does this rate cover fuel, insurance, the truck payment, and leave anything for next month? For thousands, the answer keeps getting harder.

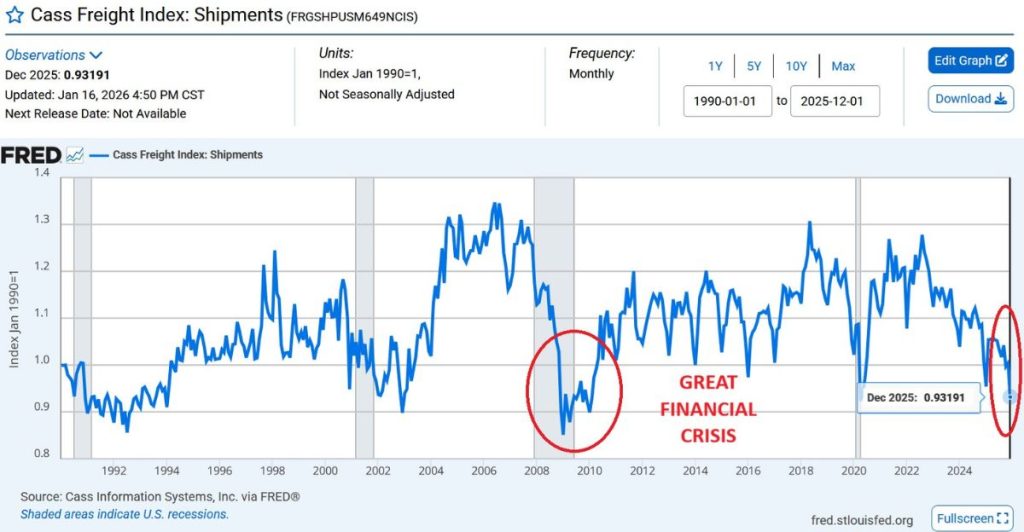

Broken Forecast

The freight recession has now humbled every forecasting model in the industry. Recovery timelines were repeatedly reset, with recovery now widely anticipated around mid‑2026 at the earliest. Each timeline reset eroded trust in the data. The January 2026 LMI reading looks like vindication, but the Cass Freight Index still showed November 2025 shipments down year‑over‑year despite month‑over‑month gains. Transportation prices can no longer serve as a reliable proxy for demand. That precedent changes how every shipper, carrier, and analyst evaluates freight cycles going forward.

Winners and Losers

Large national carriers with financial depth and shipper relationships are consolidating market share while smaller owner‑operators lose access to premium freight. The irony is sharp: the same carriers that were celebrated as “healthy market tightening” are now called a survivability crisis by the same analysts. Tariff‑related cost increases haven’t fully hit inflation data yet, but they will once pre‑tariff inventories run out. Shippers who locked intermodal contracts early look brilliant. Carriers who banked on volume returning look exposed. The freight market is picking winners, and size is the only currency.

Unfinished Cascade

The cascade isn’t slowing down. If tariffs stick, inventory normalization hits hard in the second half of 2026, potentially collapsing demand and forcing carriers to slash rates just to fill trucks. That erases every pricing gain from January. Larger carriers are already willing to undercut spot rates to lock in volume, which can trigger a collapse in pricing floors that drags everyone down. Technology providers are building modal‑agnostic routing tools that treat trucking as one option among many. The “recovery” produced higher prices, a smaller industry, and a system that keeps contracting. The next chapter writes itself.

Sources:

“January 2026 Logistics Managers’ Index Report.” Logistics Managers’ Index / Colorado State University, Feb. 2026.

“Ocean Freight Rates Fall Across Key Routes in Early 2026 Amid Capacity Uncertainty.” Global Trade Magazine, 23 Feb. 2026.

“US Trucking Rates Are Increasing — Is the Great Freight Recession Over?” AlixPartners, 24 Feb. 2026.