Good Price’ Auto Loans Hit 20–35% APR As Decade‑High Delinquencies Crush 6 Million Americans

She drove off the lot owing $21,700 on a car worth $14,000. A 2020 Chevy Equinox, financed through DriveTime at 20% APR, with $4,465 in add-ons bundled into the paperwork. Gap coverage. Extended warranty. Fabric protection. The monthly number looked survivable. The total didn’t.

Before she made a single payment, she was $7,700 underwater. And the analyst who reviewed her deal didn’t flinch at the rate. He’d seen worse. Roughly 6 million Americans with credit scores between 300 and 600 face the same math every year.

The Rate You Never Negotiated

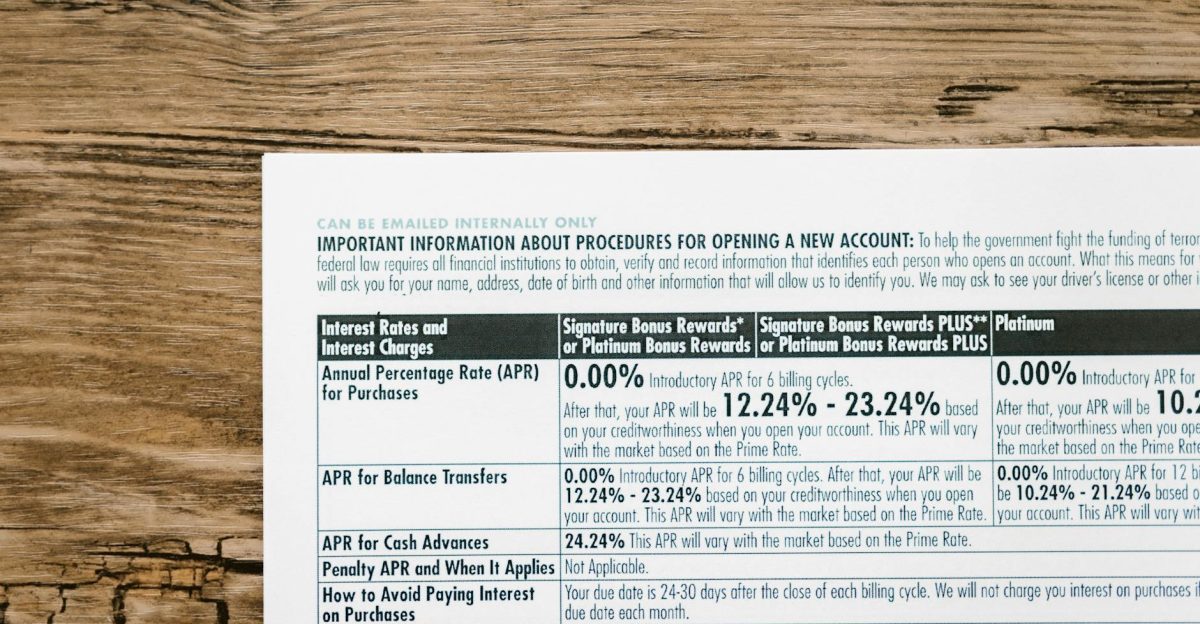

Deep subprime borrowers pay 21.85% APR on used cars. Excellent credit pays 7.70%. That gap, on a $30,000 loan over 60 months, costs roughly $9,000 in extra interest. Same car. Same highway. Completely different financial universe. But the APR printed on the contract isn’t even the real number.

Dealers mark up the lender’s “buy rate” by 1% to 2.5% and pocket the difference as “dealer reserve.” On a $35,000 loan, that invisible markup costs $1,900. The borrower never sees the original rate offered.

The Doors Slamming Shut

Most people assume bad credit just means a higher rate. Shop around, find a fair deal, move on. That assumption is collapsing. Mainstream lenders denied 15.2% of applications in October, up from 6.7% in June.

That denial rate more than doubled in roughly six months, the fastest swing since the 2008 crisis. The average credit score for used car financing hit 690 in Q2 2025. Below 640, most banks auto-decline without a human ever reading the file. The only doors still open charge admission.

The Trap Behind the Approval

Buy-here-pay-here lots now account for approximately 10.5% of all car loans. They approve almost anyone. That approval is the bait. Analyst Chris Christensen put it plainly: “Twenty percent is a good price at those places. I have seen 35% APR on car loans.” Subprime lenders start at 13% and add 3% or more in markup.

Then come the add-ons. Then the 84-month term. A $25,000 car becomes a $33,000 obligation. The payment looks affordable. The total is devastating.

The Invisible Architecture

The system has layers designed to extract money at every stage. The dealer reserve is invisible. The add-ons are presented as standard. The term length stretches payments past the car’s useful life. One affected borrower described it:

“It’s an environment where the other side has all the information, and they have all the leverage, and they have all the experience in doing these types of deals.” A prime borrower pays roughly $759 monthly on a $42,000 loan. A subprime borrower pays $777 monthly on a $25,000 loan. Same payment. Half the car.

The Numbers That Prove the Design

On a $30,000 loan over 60 months, a borrower with a 500 credit score pays approximately $550 per month. A 650-score borrower pays $470. Total interest: $13,040 versus $8,227. That $4,800 difference buys nothing. No better car. No faster payoff. Just the cost of being poor.

New cars lose 20% or more of their value in the first year. A zero-down subprime borrower is underwater before the first oil change. The financing doesn’t build equity. It destroys it.

The Delinquency Wave Already Here

Auto loan 60-day delinquencies have reached their highest level in a decade. Credit card delinquencies now exceed Great Recession peaks. Loans originated in 2022 and later are performing worse than pandemic-era loans because borrowers locked into higher rates have zero budget slack.

About 20% of borrowers approved with 720-plus credit scores in 2022-2023 have since dropped below 720, triggering refinancing failures across the board. The extraction system worked perfectly during easy money. Now the bills are arriving, and the architecture has no pressure valve.

Seven Years for One Missed Payment

Payment history accounts for 35% of a credit score. One late payment sits on a credit report for up to seven years. Miss a payment in month six of an 84-month loan, and that mark outlasts the loan itself.

This is the mechanism nobody discusses: the seven-year reporting window turns a single financial stumble into a decade of higher rates on everything. Cars, apartments, insurance. The penalty doesn’t match the crime. It multiplies it. And once 20% APR becomes “standard” for deep subprime, 25% follows. The ceiling keeps rising.

The One Exit Most People Miss

Credit unions approve borrowers that mainstream lenders auto-decline. They focus on members with FICOs under 640, pull rent and utility histories, and cap rates at 18% under NCUA limits. That’s half what BHPH lots charge for the same borrower.

The problem is scale. Credit unions lack the inventory, speed, and branch networks to absorb millions of rejected applicants. Maryland caps auto loan rates at 24% and prohibits prepayment penalties on loans over 61 months. Most states allow 28% or higher and look the other way entirely.

The System Working as Designed

Mainstream lenders deny you. BHPH dealers approve you at 20-35%. Credit unions would help but can’t keep up. The monthly payment is the decoy. Dealer reserve, bundled add-ons, 84-month terms, and seven-year credit marking are the real product.

As delinquencies climb toward levels that historically precede mass repossessions, the used car market faces a flood of inventory that could push values down further, stranding even more borrowers underwater. The people who built this system aren’t scrambling to fix it. They’re collecting the interest.

Sources:

Experian, Auto Loan Rates and Financing for 2025, 14 August 2025

Experian, Average Car Loan Interest Rates by Credit Score, 19 June 2025

Fitch Ratings via Wolf Street, Serious Delinquency Rates for Subprime & Prime Auto Loans, 16 February 2026

Federal Reserve Bank of New York (Household Debt and Credit report, auto and credit card delinquencies), latest edition 2025–2026 window

NCUA / America’s Credit Unions, NCUA Extends 18% Interest Rate Ceiling to September 2027, 8 February 2026

Bankrate, Average Auto Loan Interest Rates by Credit Score in 2026, 1 April 2026